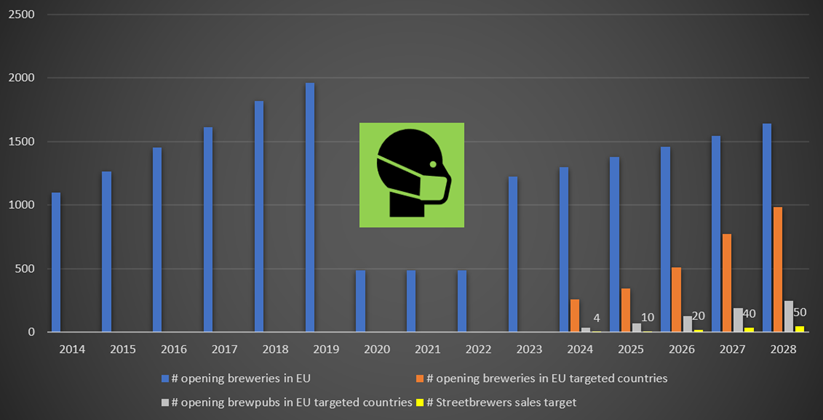

Statistics show that 40% of craft breweries are in the US, 40% in the EU and 20% elsewhere. Streetbrewers is going to focus on the European market (nearby and large enough) and analyze brewpub openings there. The quantities shown on the map below date back to 2015. In the meantime, these quantities have multiplied by 3.

Summary

Between 2014 and 2019, the number of European active breweries grew by an average of 12%. This is due to the emergence of microbreweries, which have taken 5% of the market at the expense of the large ones. In this way, Europe is copying US trends with a 10-year time lag. This growth could continue in Europe (1,500 new breweries a year), as it has for the past 10 years in the US, thanks to the emergence of brewpubs, a logical extension of consumer demand for more 'local' and 'responsible' brewing. On the one hand because craft has a future and can claim 15% of the market and on the other because a brewpup produces 5 times less than a microbrewery.

Life cycle

In details

Beginning of the century, the market of craft breweries was booming in the USA and this momentum was exported to Europe with a ten years delay.

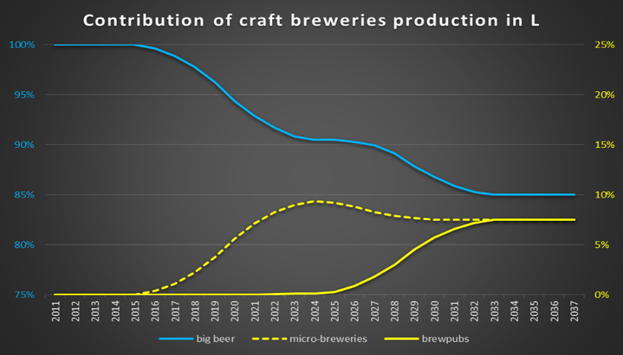

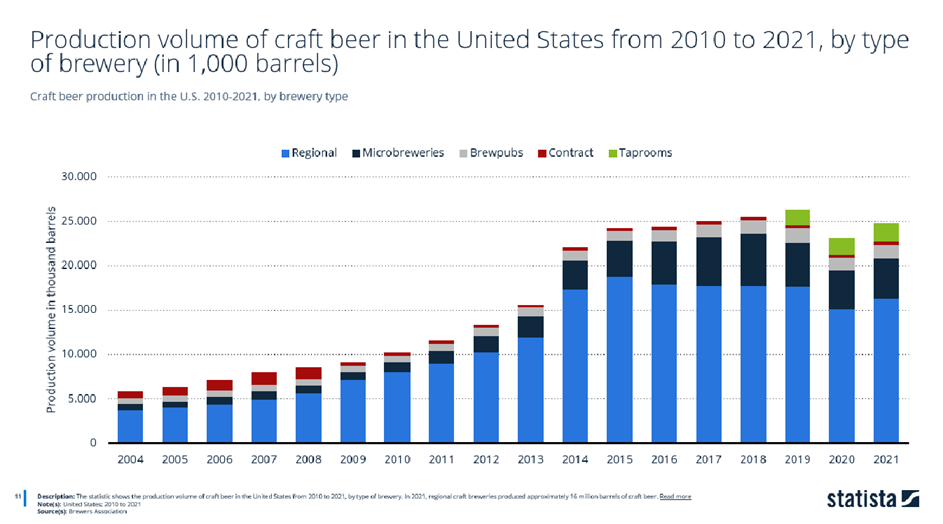

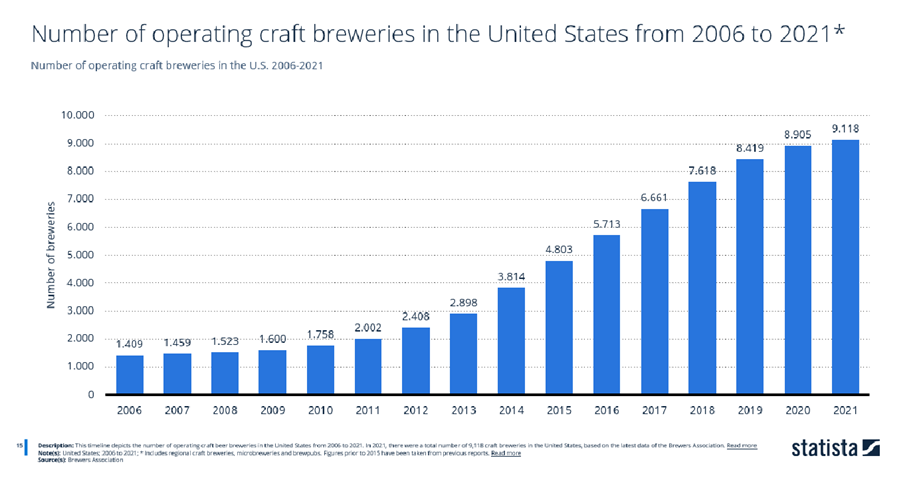

The market of craft breweries went through a first phase up to 2014 during which the number of microbreweries proliferated to the detriment of big beer (in 10 years the production of microbreweries went from 3% of total beer production to 11%, which means annual increase of 14%). Around 2014 microbreweries struck a balance size/number : the maximum size was limited by the means of distribution ( which are generally padlocked by big beer) and the minimum size limited by the profitability , usually a 1000hl/year. In 2014 craft had 11,5 (3814/330) microbreweries per million inhabitants in the USA and in 2019 the number had increased to 25 (8419/330).

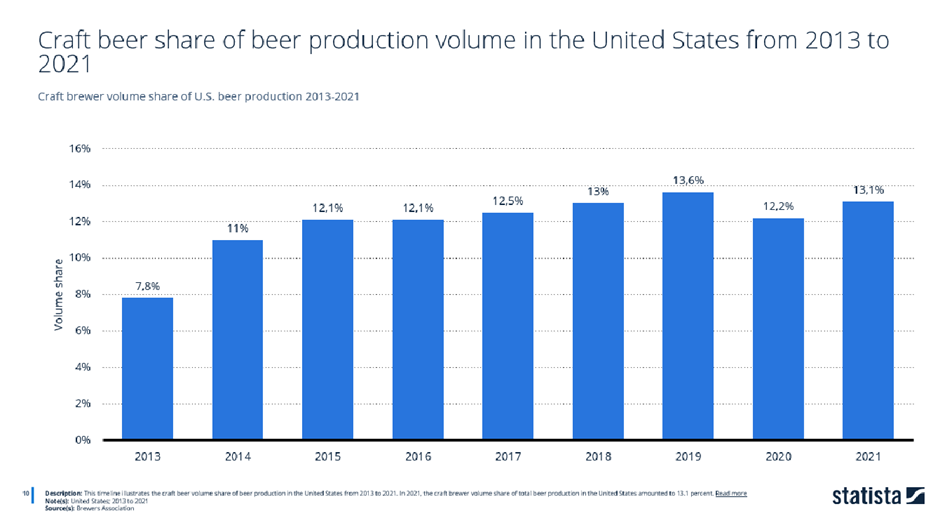

The market of craft beer then went through a second phase after 2014 with a more modest growth (% of total beer production increased from 11% in 2014 to 13,6 % in 2019, which means an annual increase of market share of 4%). At the same time an internal shift took place to even more local: from microbreweries to brewpubs. The average capacity of a brewery was nearly halved between 2014 and 2019 ( 22.000kb for 3.814 breweries versus 26.000kb for 8.419 breweries)

One can make the parallelism with Europe.

Between 2014 and 2019 the number of active breweries increased on average by 12% per year ( from 6.855 in 2014 to 12.247 in 2019), which means 24 breweries per million inhabitants ( 12.247/541). The biggest contribution in number comes from craft. Europe has reached the same order of magnitude of average density as in the USA before moving on to the second phase.

Europe can expect the same evolution as in the USA (tendency to more local) with a ten year delay ( corresponding to the delay of the explosion of craft), that means around 2024. One can effectively notice the progressive opening of brewpubs. The number of breweries in Europe will continue to grow and its rate of growth maintained because on the one hand craft has a future and can claim 15% of the market and on the other because a brewpup produces 5 times less than a microbrewery.

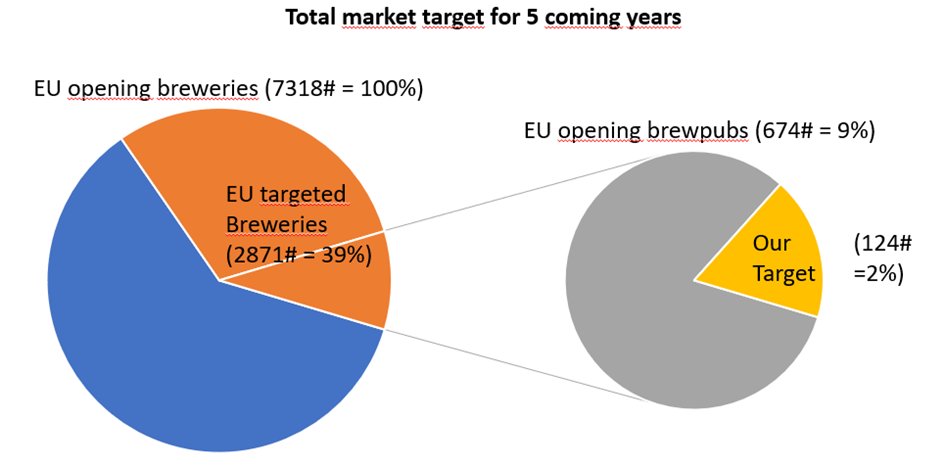

Covid has frozen the number of active breweries, therefore Streetbrewers assumes that number of breweries in 2022 equals that of 2019. We notice that activity has returned to the pre covid tendencies, but out of precaution Streetbrewers assumes a new average growth of 6% of the number of active breweries instead of 12%. We also have to add 4% for the new breweries compensating the closures and absorptions by bigger breweries. Streetbrewers targets an EU geographical coverage growing in 5 years from 20% to 60%. Streetbrewers assumes that the share of brewpubs in the new European craft will be growing from 15% to 25% in the next 5 years. Streetbrewers targets a market share (of brewpubs in selected countries) growing in 5 years from 10% to 20%.

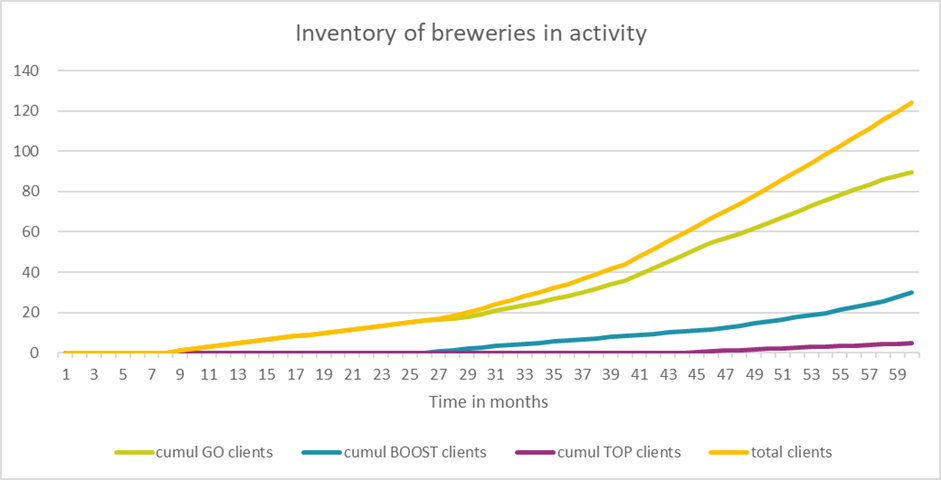

After 18 months, 2/3 of GO clients switch to BOOST version. After 18 more months, 1/2 of BOOST clients switch to TOP version. After 5 years the inventory is 89 GO customers, 30 BOOST customers & 5 TOP customers (total 124).

Go to market

Streetbrewers' first prospects will be people able to consider purchasing within 1 year :